If you’re running ads for credit products, fintech services, investment solutions, or other financial services, you’re probably familiar with this situation: your campaign is ready to launch, the deadline is tight, and suddenly your ads get stuck in review or are rejected without a clear explanation.

For brands in fintech, lending, payments, wealth management, and other financial sectors, this is one of the most common reasons for launch delays. Until ads are approved, the campaign doesn’t drive traffic, the team wastes time, and the business loses out on potential revenue.

The challenge is that financial advertising is subject to much stricter scrutiny than most other categories. Platforms classify such offers as a high-risk category and evaluate not only the creative assets but also the ad copy, landing pages, disclaimers, legal language, targeting settings, and signs of regulatory compliance.

An additional challenge is that each platform has its own set of rules. What appears acceptable on one channel may be flagged, restricted, or rejected entirely on another.

In this article, we’ll break down how to get financial ads approved on Meta, Google, and TikTok, what the platforms check first, and what steps you can take to reduce the risk of rejection before your campaign even launches.

For brands in fintech, lending, payments, wealth management, and other financial sectors, this is one of the most common reasons for launch delays. Until ads are approved, the campaign doesn’t drive traffic, the team wastes time, and the business loses out on potential revenue.

The challenge is that financial advertising is subject to much stricter scrutiny than most other categories. Platforms classify such offers as a high-risk category and evaluate not only the creative assets but also the ad copy, landing pages, disclaimers, legal language, targeting settings, and signs of regulatory compliance.

An additional challenge is that each platform has its own set of rules. What appears acceptable on one channel may be flagged, restricted, or rejected entirely on another.

In this article, we’ll break down how to get financial ads approved on Meta, Google, and TikTok, what the platforms check first, and what steps you can take to reduce the risk of rejection before your campaign even launches.

Why Financial Ads Get Rejected More Often

Meta Moderation for Financial Ads

Google Moderation for Financial Ads

TikTok Moderation for Financial Ads

Main Differences Between Platforms

Real Compliance Examples

Cross-Platform Checklist

How Digital Eagle Helps Financial Advertisers

FAQ

Meta Moderation for Financial Ads

Google Moderation for Financial Ads

TikTok Moderation for Financial Ads

Main Differences Between Platforms

Real Compliance Examples

Cross-Platform Checklist

How Digital Eagle Helps Financial Advertisers

FAQ

Why financial ads get rejected more often than other campaigns?

Financial ads are subject to stricter scrutiny because platforms classify them as high-risk. The logic here is simple: money-related offers can easily raise concerns due to misleading promises, hidden terms, predatory lending, unlicensed services, or claims that could cause financial harm to users. Therefore, such campaigns are reviewed much more closely than standard e-commerce or SaaS ads.

In many cases, ads are rejected not because the product is prohibited, but because the moderation team finds the offer too aggressive, the landing page insufficiently transparent, the disclaimers weak, or there is a mismatch between the ad copy and the page content. An additional risk factor arises when the platform cannot verify the advertiser’s status or their right to promote a financial service in the selected geographic region.

That is precisely why approval in the financial sector depends not only on the ad itself. The outcome is influenced by the entire campaign structure: ad copy, the account, the landing page, disclosure of terms and conditions, and the overall level of compliance signals.

The best way to approach financial ad moderation is platform by platform. While the same offer may look compliant at first glance, Meta, Google, and TikTok each apply their own review logic, risk signals, and approval requirements.

In many cases, ads are rejected not because the product is prohibited, but because the moderation team finds the offer too aggressive, the landing page insufficiently transparent, the disclaimers weak, or there is a mismatch between the ad copy and the page content. An additional risk factor arises when the platform cannot verify the advertiser’s status or their right to promote a financial service in the selected geographic region.

That is precisely why approval in the financial sector depends not only on the ad itself. The outcome is influenced by the entire campaign structure: ad copy, the account, the landing page, disclosure of terms and conditions, and the overall level of compliance signals.

The best way to approach financial ad moderation is platform by platform. While the same offer may look compliant at first glance, Meta, Google, and TikTok each apply their own review logic, risk signals, and approval requirements.

Source: Naukri

How does Meta review ads for financial products and services?

When financial ads are rejected by Meta, the problem is usually not a single specific word, but rather how the platform perceives the offer as a whole. For Meta, financial advertising is a category that requires heightened scrutiny, because any misleading promises, hidden terms, or overly aggressive messaging can be viewed as a risk to the user.

For brands in lending, payments, investing, insurance, and other regulated financial sectors, this adds an extra layer of complexity. Even if the product itself is legal, an ad may still get stuck in review or be rejected if the wording sounds too definitive, if key terms and conditions aren’t disclosed on the landing page, or if Meta perceives the campaign as higher risk.

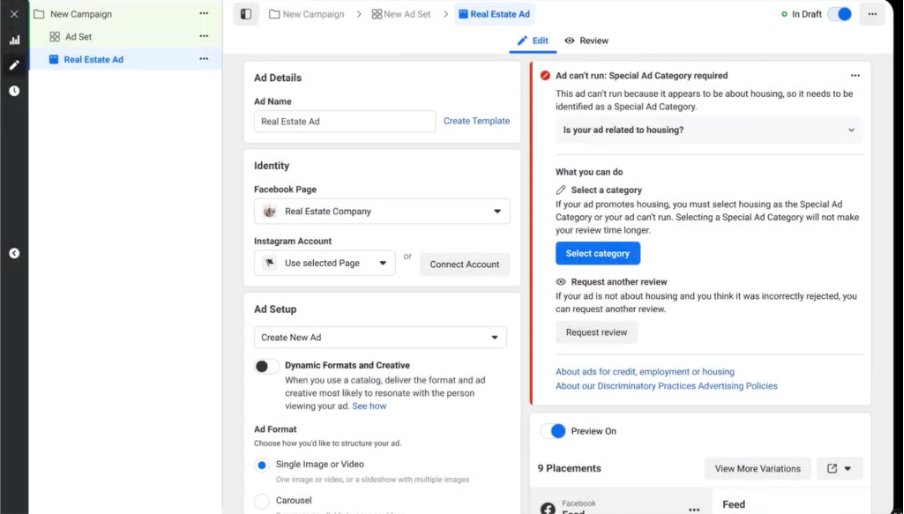

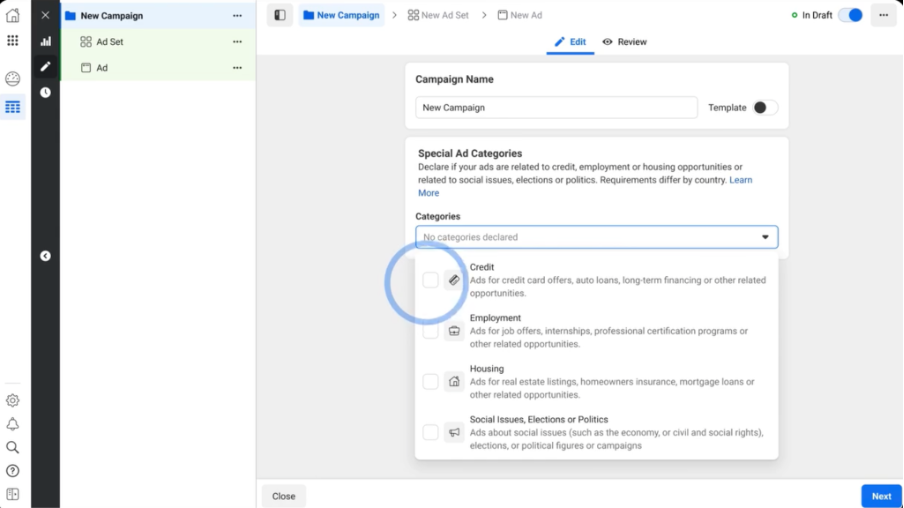

It is also important to note that Meta may impose restrictions related to sensitive targeting and platform policies. In some cases, advertisers promoting credit and related financial products need to assess separately whether their campaign falls under the Special Ad Category, particularly when it involves access to credit, financial eligibility, or similar regulated services.

An additional risk factor is a mismatch between the ad and what the user sees after clicking on it. If an ad oversimplifies the product, fails to disclose important limitations, or creates unrealistic expectations, the review system may interpret this as a policy risk.

That’s why, on Meta, it’s important to consider not only the appeal of the creative but also how transparent, consistent, and low-risk the entire ad campaign appears from the platform’s perspective. The fewer controversial signals the moderation system detects, the higher the chance of getting approved without unnecessary delays.

For brands in lending, payments, investing, insurance, and other regulated financial sectors, this adds an extra layer of complexity. Even if the product itself is legal, an ad may still get stuck in review or be rejected if the wording sounds too definitive, if key terms and conditions aren’t disclosed on the landing page, or if Meta perceives the campaign as higher risk.

It is also important to note that Meta may impose restrictions related to sensitive targeting and platform policies. In some cases, advertisers promoting credit and related financial products need to assess separately whether their campaign falls under the Special Ad Category, particularly when it involves access to credit, financial eligibility, or similar regulated services.

An additional risk factor is a mismatch between the ad and what the user sees after clicking on it. If an ad oversimplifies the product, fails to disclose important limitations, or creates unrealistic expectations, the review system may interpret this as a policy risk.

That’s why, on Meta, it’s important to consider not only the appeal of the creative but also how transparent, consistent, and low-risk the entire ad campaign appears from the platform’s perspective. The fewer controversial signals the moderation system detects, the higher the chance of getting approved without unnecessary delays.

When does the Special Ad Category apply to financial ads on Meta?

In some cases, ads for financial services on Meta may fall under the Special Ad Category framework, especially when they relate to credit products, loans, or offers connected to access to financial opportunities. Meta introduced a separate Special Ad Category for Financial Products and Services, replacing the former credit category. For these campaigns, the platform applies additional audience and targeting restrictions. For advertisers based in the United States — or targeting audiences there — use of this category became mandatory for relevant financial ads starting January 21, 2025. For advertisers, this means additional targeting limitations and a stricter approach to campaign setup review.

Therefore, when promoting credit-related offers, it’s important to check in advance not only the creative and landing page, but also whether the campaign setup complies with Meta’s guidelines for sensitive categories.

Therefore, when promoting credit-related offers, it’s important to check in advance not only the creative and landing page, but also whether the campaign setup complies with Meta’s guidelines for sensitive categories.

Source: Facebook

What usually gets financial ads rejected on Meta?

In practice, Meta most often rejects financial ads not because of the fact that a financial product is being promoted, but because of how the offer is presented in the ad and on the landing page. One of the most common triggers is overly strong promises in the ad copy. If the ad gives the impression of guaranteed approval, easy profits, quick earnings, or simple access to money without conditions or restrictions, this can be perceived as a misleading claim.

In practice, phrases like the following create additional risk on Meta:

Such phrasing is risky not only because it makes overly strong promises, but also because it can sound like misleading claims or an appeal to the user’s personal attributes—such as their debts, credit history, or financial situation. It is much safer to use more neutral language: for example, inviting users to review the available terms, eligibility criteria, rates, fees, and a full product description on the website.

The second critical area is the landing page. Even if the ad itself looks polished, the campaign may be rejected if, after clicking, the user does not see a clear description of the product, key terms, restrictions, fees, APR, eligibility criteria, or other important details. For Meta, this is a sign that the offer is not disclosed honestly and fully enough.

A separate risk relates to personal attributes. If an ad sounds as though the brand knows the user’s financial situation, debts, credit status, or other sensitive characteristics, this could trigger a policy flag. For Meta, this is one of the most sensitive triggers in financial services advertising.

In practice, phrases like the following create additional risk on Meta:

- "Get approved in minutes"

- "Bad credit? We’ll approve you anyway"

- "Quick cash with no strings attached"

- "A guaranteed solution to your financial problems"

Such phrasing is risky not only because it makes overly strong promises, but also because it can sound like misleading claims or an appeal to the user’s personal attributes—such as their debts, credit history, or financial situation. It is much safer to use more neutral language: for example, inviting users to review the available terms, eligibility criteria, rates, fees, and a full product description on the website.

The second critical area is the landing page. Even if the ad itself looks polished, the campaign may be rejected if, after clicking, the user does not see a clear description of the product, key terms, restrictions, fees, APR, eligibility criteria, or other important details. For Meta, this is a sign that the offer is not disclosed honestly and fully enough.

A separate risk relates to personal attributes. If an ad sounds as though the brand knows the user’s financial situation, debts, credit status, or other sensitive characteristics, this could trigger a policy flag. For Meta, this is one of the most sensitive triggers in financial services advertising.

What does Meta check on the landing page and in the campaign settings?

Meta evaluates not only the ad copy itself, but also how consistent and transparent the entire user journey appears. The landing page must clearly explain what product is being promoted, under what terms it is available, and what restrictions or mandatory disclosures apply. If the ad and landing page create different expectations, the likelihood of rejection increases significantly.

In addition, it’s important to consider targeting restrictions in the financial category. Depending on the type of offer, Meta may restrict certain age settings, audience options, or other parameters that are standard in regular campaigns. Therefore, campaign setup for sensitive categories should always be reviewed individually rather than using a template.

In addition, it’s important to consider targeting restrictions in the financial category. Depending on the type of offer, Meta may restrict certain age settings, audience options, or other parameters that are standard in regular campaigns. Therefore, campaign setup for sensitive categories should always be reviewed individually rather than using a template.

How can you improve the approval chances of financial ads on Meta?

To increase your chances of approval, it’s important to view Meta financial ads as a system rather than as individual creatives. Before launching, you should check a few things:

If financial ads are regularly rejected, the problem often lies not in a single element, but in the overall compliance logic of the campaign. That is why, on Meta, it is not the most "flashy" ads that perform best, but those that appear clear, transparent, and low-risk for both the user and the platform.

If Meta is particularly sensitive to audience restrictions, Special Ad Category logic, and personal attributes, Google adds another layer of complexity through verification, certification, and market-specific financial advertising rules.

- Does the copy contain any overly strong or absolute promises?

- Does the ad sound as if the brand knows the user’s personal financial situation?

- Does the message in the ad match what the user sees on the landing page?

- Are key terms, conditions, restrictions, and disclaimers disclosed on the page?

- Does the campaign fall under a Special Ad Category?

- Does the targeting setup comply with Meta’s rules for sensitive categories?

- Does the entire offer appear transparent and credible from the platform’s perspective?

If financial ads are regularly rejected, the problem often lies not in a single element, but in the overall compliance logic of the campaign. That is why, on Meta, it is not the most "flashy" ads that perform best, but those that appear clear, transparent, and low-risk for both the user and the platform.

If Meta is particularly sensitive to audience restrictions, Special Ad Category logic, and personal attributes, Google adds another layer of complexity through verification, certification, and market-specific financial advertising rules.

Useful links:

How does Google review ads for financial products and services?

For financial ads on Google, the key factor in approval is often not the creative itself, but passing the mandatory financial services verification. Depending on the product and geographic region, advertisers may face not only standard moderation but also additional requirements for verification, certification, and confirmation of their right to promote financial services in a specific country.

For brands in lending, personal finance, investing, payments, and related verticals, this means that ad approval on Google depends on more than just the creative and ad copy. The platform evaluates not only the ad copy and landing page, but also the advertiser’s status, certification status, offer transparency, and the completeness of required disclosures.

For brands in lending, personal finance, investing, payments, and related verticals, this means that ad approval on Google depends on more than just the creative and ad copy. The platform evaluates not only the ad copy and landing page, but also the advertiser’s status, certification status, offer transparency, and the completeness of required disclosures.

Source: Google Ads Help

When is verification required for financial ads on Google?

It is important to understand that, in many cases, financial services verification is tied not just to the account as a whole, but to specific target markets. Each target location may require separate verification, and the application must typically be submitted by an authorized representative. During the process, Google may request information about the type of financial services, licenses, the company’s registration number, and other data confirming the brand’s right to operate in the selected jurisdiction.

In practice, this means that before launching a campaign, it’s important to check the requirements for your specific geographic region and product type in advance. If verification is required but hasn’t been completed, your ad may not be approved, regardless of the quality of the creative and landing page.

In practice, this means that before launching a campaign, it’s important to check the requirements for your specific geographic region and product type in advance. If verification is required but hasn’t been completed, your ad may not be approved, regardless of the quality of the creative and landing page.

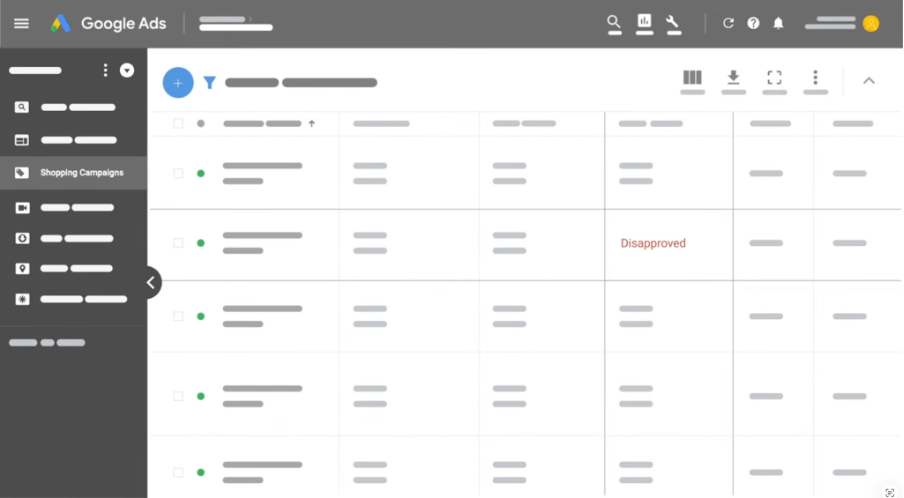

What are the most common mistakes that lead to a rejection by Google?

When financial campaigns get stuck in Google’s review process, the problem is often more complex than just "poor ad copy." Google applies stricter review criteria to financial products because these offers involve money, loans, investments, and other decisions that can impact a user’s well-being.

One of the most common reasons for rejection is the lack of required verification or an incomplete certification process. For Google, this is one of the most common deal-breakers: if an advertiser is not properly verified, paid advertising may be restricted even before the creative itself is reviewed.

Another common issue is a lack of transparency in the offer terms. It is critical for Google that the landing page clearly outlines the key product details: fees, APR, terms, restrictions, eligibility criteria, and other important details. If a user cannot quickly understand exactly what is being offered and under what terms, this increases the risk of disapproval.

Another area of risk is overly strong claims. Promises such as "instant approval," "easy money," "guaranteed returns," or overly simplified descriptions of complex financial products may be perceived as misleading advertising. Credit products, high-interest loans, and other offers remain particularly sensitive areas where Google expects stricter disclosure of details.

For example, in the U.S., Google explicitly restricts advertising for personal loans: the platform does not allow the promotion of loans with an APR of 36% or higher. In addition, for permitted personal loans, Google requires that the full repayment term be at least 61 days and that the key terms of the loan be clearly disclosed on the landing page or in the app.

One of the most common reasons for rejection is the lack of required verification or an incomplete certification process. For Google, this is one of the most common deal-breakers: if an advertiser is not properly verified, paid advertising may be restricted even before the creative itself is reviewed.

Another common issue is a lack of transparency in the offer terms. It is critical for Google that the landing page clearly outlines the key product details: fees, APR, terms, restrictions, eligibility criteria, and other important details. If a user cannot quickly understand exactly what is being offered and under what terms, this increases the risk of disapproval.

Another area of risk is overly strong claims. Promises such as "instant approval," "easy money," "guaranteed returns," or overly simplified descriptions of complex financial products may be perceived as misleading advertising. Credit products, high-interest loans, and other offers remain particularly sensitive areas where Google expects stricter disclosure of details.

For example, in the U.S., Google explicitly restricts advertising for personal loans: the platform does not allow the promotion of loans with an APR of 36% or higher. In addition, for permitted personal loans, Google requires that the full repayment term be at least 61 days and that the key terms of the loan be clearly disclosed on the landing page or in the app.

What should you check before launching a Google Ads campaign?

Before launching financial ads on Google, it’s important to ensure that your campaign is ready not only from a marketing perspective but also in terms of compliance. First, you should check whether financial services verification is required for your market and whether all necessary certification steps have been completed. Next, you need to ensure that the ads and landing page consistently convey the essence of the product, and that all key terms and conditions are readily available to the user without requiring additional searching.

Special attention should be paid to legal wording and disclosures. In financial advertising, Google expects a higher level of transparency than in most other categories, so even strong, performance-focused creative cannot compensate for a landing page that is unclear or legally flawed.

Special attention should be paid to legal wording and disclosures. In financial advertising, Google expects a higher level of transparency than in most other categories, so even strong, performance-focused creative cannot compensate for a landing page that is unclear or legally flawed.

How can you improve the approval chances of financial ads on Google?

To increase the likelihood of approval, it’s a good idea to review the entire campaign against a compliance checklist before launching it:

If financial ads are regularly getting rejected on Google, the issue often lies not in performance marketing itself, but in insufficient verification or a weak disclosure setup.

- Check whether financial services verification or certification is required for the selected region;

- Ensure that verification is completed before launch;

- Remove overly absolute claims from the ad copy;

- Disclose the APR, fees, terms, restrictions, and other key conditions on the landing page;

- Verify that the message in the ad matches the page content;

- Ensure that the product does not fall into prohibited or strictly restricted subcategories;

- Make the brand and offer as transparent as possible for the user and the platform.

If financial ads are regularly getting rejected on Google, the issue often lies not in performance marketing itself, but in insufficient verification or a weak disclosure setup.

Useful links:

How does TikTok review ads for financial products and services?

TikTok’s review logic is different again. Beyond policy compliance, the platform is especially sensitive to licensing signals, age restrictions, and whether a financial offer feels overly promotional or too good to be true.

TikTok explicitly states that ads for financial services require enhanced transparency. The platform’s general guidelines specifically emphasize that advertisers must comply with local laws and regulatory requirements, obtain a license from local or regional authorities if necessary, use appropriate disclaimers, and restrict ad views to audiences aged 18 and older.

For financial brands, this means that approval on TikTok depends on more than just the quality of the creative. Even a high-performing campaign can be rejected if the product falls into a restricted category, the landing page lacks transparency, or the platform has doubts about the advertiser’s regulatory legitimacy.

TikTok explicitly states that ads for financial services require enhanced transparency. The platform’s general guidelines specifically emphasize that advertisers must comply with local laws and regulatory requirements, obtain a license from local or regional authorities if necessary, use appropriate disclaimers, and restrict ad views to audiences aged 18 and older.

For financial brands, this means that approval on TikTok depends on more than just the quality of the creative. Even a high-performing campaign can be rejected if the product falls into a restricted category, the landing page lacks transparency, or the platform has doubts about the advertiser’s regulatory legitimacy.

Source: TikTok Ads Policy

What is the most common reason for financial ads being rejected on TikTok?

One of the most common reasons for rejection is an offer description that isn’t transparent enough. If an ad promises easy access to money, quick results, or high returns without explaining the terms and conditions, or if it presents a complex financial product as an overly simple solution, this can be perceived as misleading messaging.

TikTok explicitly prohibits get-rich-quick schemes, "too-good-to-be-true" financial promotions, and similar schemes where a financial product is presented as an overly easy, quick, or nearly risk-free way to make money or a profit. Therefore, creatives and copy with phrases like "make money fast", "get money without hassle" or "start earning right away with no risk" are particularly dangerous on TikTok.

The second critical area is verifying the legitimacy of the product and the advertiser. For certain financial categories, TikTok may require the brand to provide proof of a license, operating permit, or other evidence of regulatory compliance. If the platform lacks sufficient confidence that the offer is being promoted legally, the risk of rejection increases significantly.

Another common issue is the landing page. Even if the ad itself appears acceptable, the campaign may not pass moderation if, after clicking on it, the user does not receive a clear explanation of the product and does not see key terms, restrictions, disclaimers, or important information about the risks and cost of the service.

TikTok explicitly prohibits get-rich-quick schemes, "too-good-to-be-true" financial promotions, and similar schemes where a financial product is presented as an overly easy, quick, or nearly risk-free way to make money or a profit. Therefore, creatives and copy with phrases like "make money fast", "get money without hassle" or "start earning right away with no risk" are particularly dangerous on TikTok.

The second critical area is verifying the legitimacy of the product and the advertiser. For certain financial categories, TikTok may require the brand to provide proof of a license, operating permit, or other evidence of regulatory compliance. If the platform lacks sufficient confidence that the offer is being promoted legally, the risk of rejection increases significantly.

Another common issue is the landing page. Even if the ad itself appears acceptable, the campaign may not pass moderation if, after clicking on it, the user does not receive a clear explanation of the product and does not see key terms, restrictions, disclaimers, or important information about the risks and cost of the service.

Source: TikTok Ads Policy

What should you check before running financial ads on TikTok?

Before launching a financial campaign on TikTok, it’s important to start by verifying product eligibility for the specific market. Next, you should assess whether the launch requires proof of license, whitelisting, or other forms of verification. After that, you should ensure that the ad copy, visual presentation, and landing page are consistent with one another and do not create misleading expectations.

Special attention should be paid to the wording. In TikTok financial ads, it’s best to avoid language that comes across as too aggressive, sensational, or promises unlimited results. The clearer, more neutral, and more transparent the offer appears, the higher the chance it will pass review without unnecessary delays.

Special attention should be paid to the wording. In TikTok financial ads, it’s best to avoid language that comes across as too aggressive, sensational, or promises unlimited results. The clearer, more neutral, and more transparent the offer appears, the higher the chance it will pass review without unnecessary delays.

How can you improve the approval chances of financial ads on TikTok?

To increase your chances of approval, it’s a good idea to go through a basic checklist before launching:

If TikTok consistently rejects financial ads, the issue is often not related to a single creative asset, but rather to insufficient compliance with policies across the entire campaign.

- Check whether the product is approved for promotion in the target region;

- Ensure that the brand has proof of license or other compliance documents, if necessary;

- Remove overly strong claims and promises of "easy" benefits;

- Disclose key terms, restrictions, and disclaimers on the landing page;

- Verify that the message in the ad matches the page content;

- Ensure that the creative does not appear to be a pressure-based or misleading offer;

- Ensure the tone of voice is appropriate, without pressure or manipulative promises

- Make the entire user journey as transparent as possible from the platform’s perspective.

If TikTok consistently rejects financial ads, the issue is often not related to a single creative asset, but rather to insufficient compliance with policies across the entire campaign.

Useful links:

What is the main difference between Meta, Google, and TikTok moderation?

In practice, the three platforms focus on different risk signals. Meta is especially sensitive to Special Ad Category eligibility, audience restrictions, ad-to-landing consistency, and personal attributes language. Google is often stricter on advertiser verification, certification, and market-specific financial services eligibility. TikTok puts more weight on licensing, age-gating to 18+, disclosure quality, and whether the offer feels sensational, misleading, or too good to be true.

Real compliance examples: what often causes rejection in practice

A financial ad can be rejected even when the product itself is legal. In practice, the most common issues look like this:

❌ The ad says "instant approval", but the landing page includes eligibility limits and manual review. That creates an ad-to-landing mismatch.

❌ The ad promises "low-cost financing", but fees, APR, or repayment terms are not clearly disclosed on the page. That weakens transparency.

❌ The copy implies the advertiser knows the user’s financial situation, such as debt, poor credit, or lack of funds. That is especially risky on Meta.

❌ The campaign is launched before verification or certification is completed, which is a common approval blocker on Google.

❌ The advertiser treats TikTok like a pure hype channel and uses sensational money language, even though the platform requires enhanced transparency and restricts these offers to adult audiences.

❌ The ad says "instant approval", but the landing page includes eligibility limits and manual review. That creates an ad-to-landing mismatch.

❌ The ad promises "low-cost financing", but fees, APR, or repayment terms are not clearly disclosed on the page. That weakens transparency.

❌ The copy implies the advertiser knows the user’s financial situation, such as debt, poor credit, or lack of funds. That is especially risky on Meta.

❌ The campaign is launched before verification or certification is completed, which is a common approval blocker on Google.

❌ The advertiser treats TikTok like a pure hype channel and uses sensational money language, even though the platform requires enhanced transparency and restricts these offers to adult audiences.

Examples of risky vs safer financial ad wording

Risky ❌ :

Safer ✅ :

- "Get approved in minutes"

- "Bad credit? We’ll approve you anyway"

- "Guaranteed returns"

- "Fast money with no hassle"

Safer ✅ :

- "Check available options and full terms"

- "Review eligibility criteria before applying"

- "See rates, fees, and repayment details"

- "Explore regulated financial solutions in your market"

Cross-Platform Checklist: What to Check Before Launching Financial Ads

Regardless of the platform, financial ads are more likely to pass moderation when the advertiser prepares not only the creative assets but the entire advertising campaign. In practice, most issues stem from recurring factors: opaque offers, poor landing pages, incomplete disclaimers, overly bold promises, or a lack of verification and compliance signals.

Before launching a campaign, it’s a good idea to go through a basic checklist:

The less ambiguity there is in the ad campaign, the higher the chance of getting approved without unnecessary delays.

Before launching a campaign, it’s a good idea to go through a basic checklist:

- check whether the product is approved for promotion in the selected region;

- make sure all required verification or certification steps have been completed, if required by the platform;

- remove overly strong claims and promises of guaranteed results;

- check the copy for misleading wording or phrases that create unrealistic expectations;

- make sure the ad and landing page convey the same message;

- disclose key terms on the page: fees, APR, restrictions, eligibility criteria, etc.

- disclose key terms on the page: fees, APR, restrictions, eligibility criteria, and risks;

- add clear disclaimers where necessary;

- check whether the ad uses personal attributes or sensitive language;

- ensure that targeting and campaign setup comply with sensitive categories rules;

- make the brand, product, and terms as transparent as possible for the user and the platform;

- the entire campaign is tailored to the specific platform logic, rather than assembled using a generic template.

The less ambiguity there is in the ad campaign, the higher the chance of getting approved without unnecessary delays.

When the problem is not just the creative

If financial ads are regularly held up in review, receive repeated rejections, or face restrictions on various platforms, the issue often runs deeper than just the ad copy. In such cases, it’s important to review not only the copy but also the entire moderation and compliance setup: category selection, disclosure logic, landing page transparency, verification status, and policy alignment across platforms.

How Digital Eagle helps financial advertisers reduce moderation risk

If your team needs to launch financial campaigns faster and with a lower risk of rejection, Digital Eagle can help with moderation and compliance support across Meta, Google, and TikTok.

For teams in lending, fintech, payments, investing, and other sensitive categories, support often starts before launch — with campaign review, landing page checks, category alignment, disclosure logic, and platform-specific compliance preparation.

Depending on the task, Digital Eagle can help with:

For teams working in lending, fintech, payments, investing, and other sensitive financial categories, this approach helps not just "fix ads," but build a more stable launch process across platforms.

For teams in lending, fintech, payments, investing, and other sensitive categories, support often starts before launch — with campaign review, landing page checks, category alignment, disclosure logic, and platform-specific compliance preparation.

Depending on the task, Digital Eagle can help with:

- pre-launch review of financial campaigns before they are submitted for moderation;

- reviewing ad copy, creatives, and landing pages for policy risks;

- identifying issues in campaign setup, category selection, and targeting logic;

- preparing campaigns for stricter platform requirements across Meta, Google, and TikTok;

- support with moderation and compliance issues in complex financial verticals;

- reducing the risk of repeated rejections and launch delays.

For teams working in lending, fintech, payments, investing, and other sensitive financial categories, this approach helps not just "fix ads," but build a more stable launch process across platforms.

F.A.Q.

Why are financial ads rejected even when they come from legitimate brands?

Because the platform evaluates not only the product’s legal status, but also how transparently and accurately it is presented in the ad, on the landing page, and in the campaign setup.

Because the platform evaluates not only the product’s legal status, but also how transparently and accurately it is presented in the ad, on the landing page, and in the campaign setup.

Why does Meta keep rejecting my financial ads?

Most often, the problem isn’t with the product itself, but with how the offer is presented in the ad and on the landing page. The most common reasons include overly strong claims, references to personal attributes, terms and conditions that aren’t transparent enough, and a mismatch between the ad and the landing page.

Most often, the problem isn’t with the product itself, but with how the offer is presented in the ad and on the landing page. The most common reasons include overly strong claims, references to personal attributes, terms and conditions that aren’t transparent enough, and a mismatch between the ad and the landing page.

How long does Google Financial Services verification take?

The timeframe depends on the market, the type of product, and the completeness of the documentation. Therefore, it’s best to start the verification process early, even before finalizing the launch timeline, to ensure that approval doesn’t hold up the campaign launch at the last minute.

The timeframe depends on the market, the type of product, and the completeness of the documentation. Therefore, it’s best to start the verification process early, even before finalizing the launch timeline, to ensure that approval doesn’t hold up the campaign launch at the last minute.

Do you need a license to run fintech ads on TikTok?

In many cases, TikTok requires advertisers to verify the legality of their business and their right to promote financial services in a specific region. For certain categories, this may include proof of licensing or other compliance documents.

In many cases, TikTok requires advertisers to verify the legality of their business and their right to promote financial services in a specific region. For certain categories, this may include proof of licensing or other compliance documents.

What disclaimers are required for financial ads?

It depends on the product and market, but in general, the platform expects that key terms, restrictions, fees, APRs, risks, and eligibility criteria be disclosed transparently and unambiguously.

It depends on the product and market, but in general, the platform expects that key terms, restrictions, fees, APRs, risks, and eligibility criteria be disclosed transparently and unambiguously.

Can I appeal the rejection of a financial ad?

Yes, in some cases an appeal is possible. However, in practice, it’s best to first identify the root cause of the rejection: the issue may lie not only in the creative, but also in the landing page, verification, targeting setup, or platform-specific compliance requirements.

Yes, in some cases an appeal is possible. However, in practice, it’s best to first identify the root cause of the rejection: the issue may lie not only in the creative, but also in the landing page, verification, targeting setup, or platform-specific compliance requirements.

When should a team reach out for moderation support?

It usually makes sense to do so if a campaign is regularly being rejected, approvals are taking too long, the launch depends on deadlines, or the team needs to adapt more quickly to policy requirements across multiple platforms at once.

It usually makes sense to do so if a campaign is regularly being rejected, approvals are taking too long, the launch depends on deadlines, or the team needs to adapt more quickly to policy requirements across multiple platforms at once.

Does Digital Eagle only help with creatives?

No. Support can include not only reviewing ad copy and creatives, but also checking landing pages, disclosure logic, campaign setup, category selection, and other elements that affect approval.

No. Support can include not only reviewing ad copy and creatives, but also checking landing pages, disclosure logic, campaign setup, category selection, and other elements that affect approval.